Claims-made insurance policies offer essential protection for professionals, but understanding how timing affects coverage is key to avoiding costly gaps.

A claims-made policy means that the Insurer will only pay out a claim if the policy is still active when you make the claim. If the policy expires and isn't renewed, your coverage is gone.

For a claim to be paid:

- The policy must cover the time when the incident occurred

- The policy must be active when you make the claim

Claims-made policies are used in industries that deal with professional liability and have non-obvious risks that may not surface until long after the work is done, such as advisors, consultants, developers, and healthcare.

The most common types of policies that are 'written on' a claims-made basis are:

- Professional Indemnity

- Directors and Officers Liability

- Employment Practices Liability

- Cyber Liability

- Medical Malpractice

- Environmental Liability

For these types of claims-made policies, it is essential that there are no breaks in coverage—having an active policy when the incident happens isn't enough, it only counts if you have it when you need to make a claim.

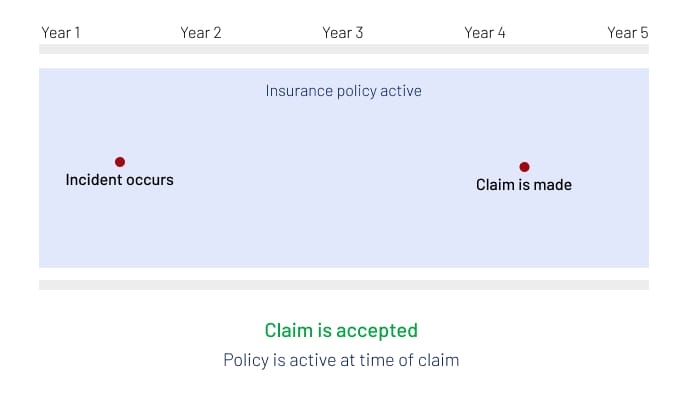

In the example above, the claim is accepted because both criteria were met: the policy was active when the incident occurred and active when the claim was made.

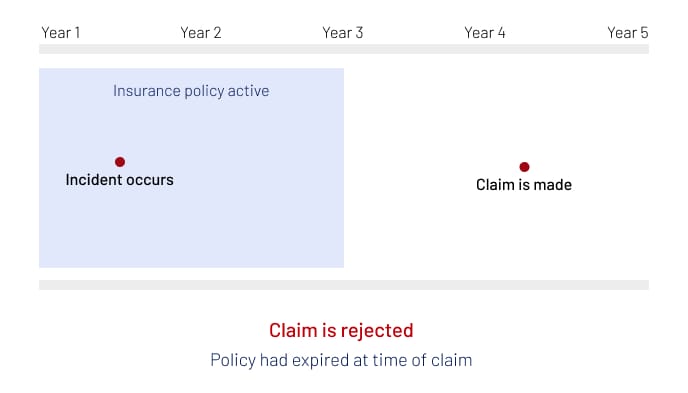

Whereas in this example, the claim is not accepted. While the policy was active when the incident occurred, it was not active when the claim was made.

Run-off coverage

Also known as "tail coverage", run-off coverage comes in to play when you need to cancel your claims-made policy but still need protection against incidents that occurred when the policy was active.

A classic example of this is retirement. When retiring, many people make the mistake of cancelling their policy without realising they still need protection. Just because you've retired doesn't mean you aren't liable for incidents that may have occurred in the closing years of your business. And to re-iterate: if the policy is no longer active, you can't make a claim.

Run-off coverage is made for situations like retirement or a business merger. You will continue to be covered for incidents that occurred while the policy was active and will be able to make claims.

Continuous coverage

Another concept that is relevant to claims-made insurance is "continuous coverage". For maximum coverage, it is essential that there are no lapses in coverage: your coverage should be continuous.

This is most relevant when swapping Insurers on the same type of policy. It may be tempting to swap to a new Insurer with a cheaper premium, but if the new policy doesn't cover the same period of time as the old policy, you may be exposing yourself to risk.

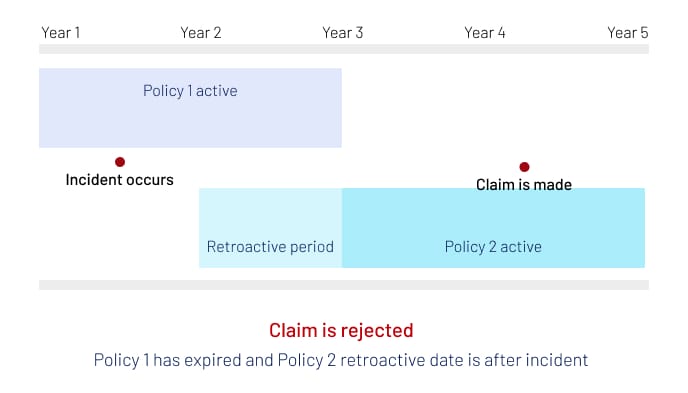

To back-date cover, claims-made policies may have a specified "retroactive date", which means they will cover any incident after that date. If unspecified, the retroactive date is typically unlimited.

In the example above, the retroactive date of the new policy does not cover when the incident occurred, so the claim will be rejected. This is an example of when 'continuous coverage' is not provided.

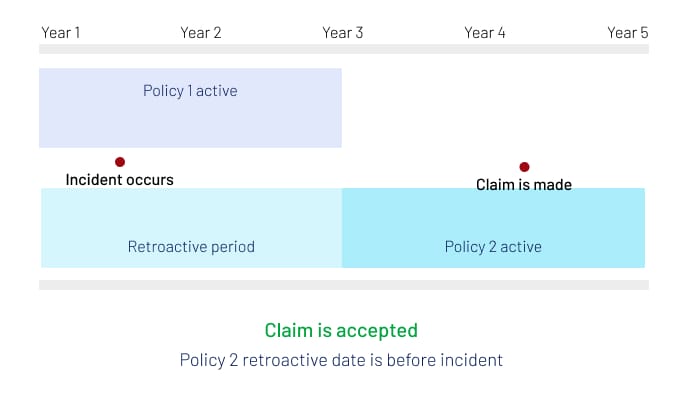

Whereas in this example, the retroactive period covers when the incident occurred.

Common mistakes

There are several common traps that businesses fall into relating to claims-made policies, most of which can be solved with run-off coverage.

Retirement

As mentioned earlier in this article, if you cancel your policy when you retire without having run-off coverage, you may find yourself without a policy to protect you for incidents that occurred while your business was active.

Mergers and Acquisitions

The same concept applies to mergers or acquisitions. If you sell your business, you are still liable for the actions of the business while you were the owner. The solution is also the same: run-off coverage.

Reduced Service

If your business changes or reduces your service offerings, you still need coverage in place for any discontinued services. You are still liable for the consequences of those services for the time that you did offer them.

Increasing insurance to secure a big deal

It's common for large business deals to have conditions requiring both parties to have insurance policies in place for up to 7 years for the deal to proceed. Many business owners are happy to increase their coverage, and premiums, in order to secure the big deal. What they often don't realise is that the increased insurance premiums aren't temporary. They can't just cancel the policy when the work is finished or they lose coverage entirely and violate the contract. They need to maintain the higher level of insurance. And quite often, those extra years of increased premiums will eat away any profit from their "big deal".

Conclusion

Claims-made policies offer essential protection for professionals and businesses exposed to long-tail risks, but they require careful management. Coverage is only triggered when both the incident and the claim occur within an active policy period, making continuous coverage and run-off arrangements critical.

Whether you're retiring, restructuring, or switching insurers, understanding the mechanics of claims-made insurance helps avoid costly gaps and ensures you're protected when it matters most.

If you're unsure whether your current policy meets your long-term needs, speak with your broker to review your coverage and explore options for run-off or retroactive protection. The right advice today can safeguard your future tomorrow.

The information on this page is intended for general educational purposes and necessarily simplifies some concepts for clarity. Insurance policies can differ widely between insurers, policy types, and jurisdictions. For guidance on your specific circumstances, you should review your policy documents carefully and consult a qualified insurance adviser, broker, or legal professional.